CONSUMERS BANCORP, INC. ANNOUNCES FIRST QUARTER FY 2026 EARNINGS

Consumers Bancorp, Inc. Reports:

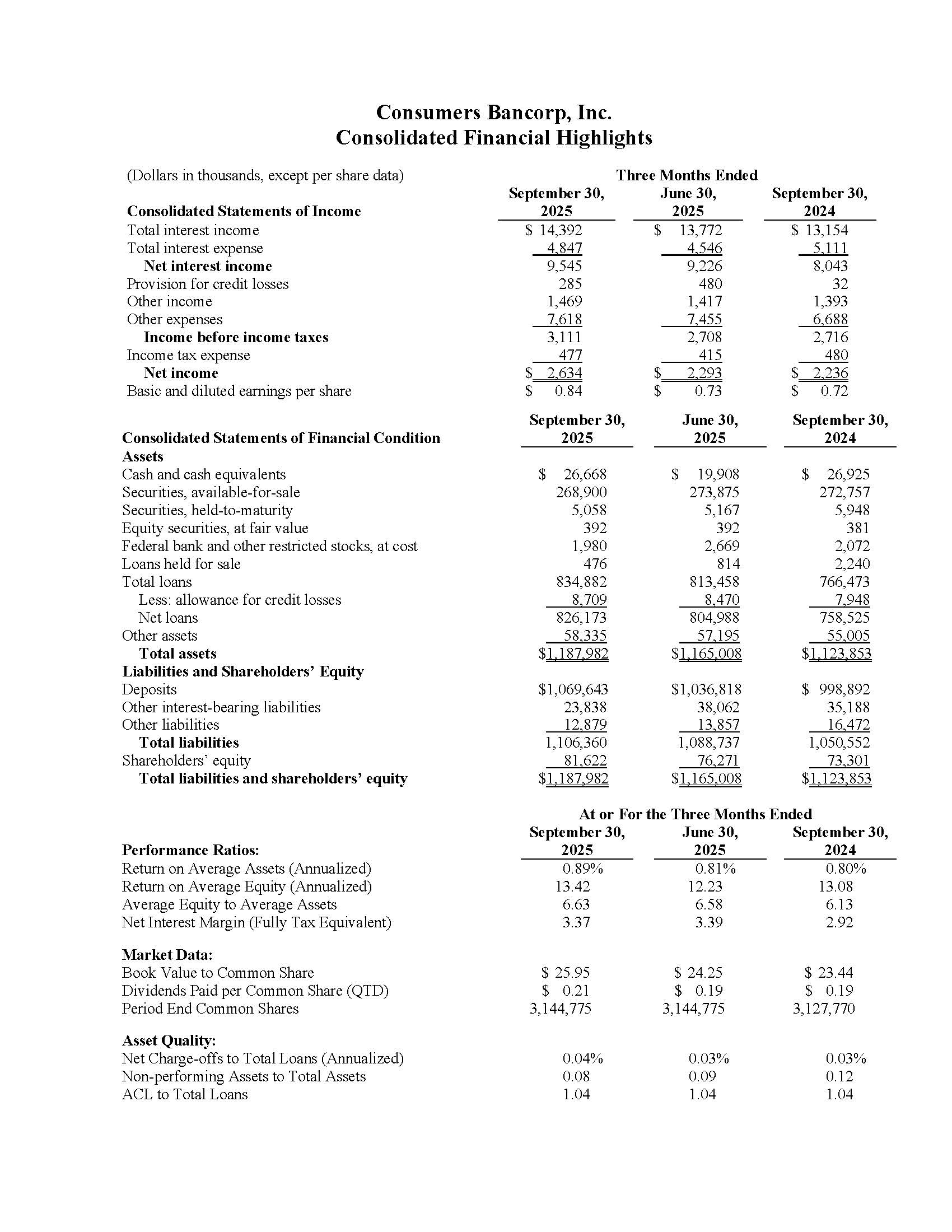

- Net income increased by $398 thousand, or 17.8%, to $2.6 million for the three-month period ended September 30, 2025 compared with the same period last year.

- Net interest income increased by $1.5 million, or 18.7%, for the three-month period ended September 30, 2025 compared with the same period last year.

- Total loans increased by $21.4 million, or an annualized 10.5%, for the three-month period ended September 30, 2025.

- Non-performing loans to total loans were 0.12%, of which 0.04% represents the government guaranteed portion, as of September 30, 2025.

- Total deposits increased by $32.8 million, or an annualized 12.7%, for the three-month period ended September 30, 2025.

- Book value increased by $1.70 per share to $25.95 per share as of September 30, 2025 from $24.25 per share as of June 30, 2025.

Minerva, Ohio—October 17, 2025 (OTCQX: CBKM) Consumers Bancorp, Inc. (Consumers) today reported net income of $2.6 million for the first quarter of fiscal year 2026, an increase of $341 thousand, or 14.9%, from the previous quarter ended June 30, 2025, and an increase of $398 thousand, or 17.8%, from the quarter ended September 30, 2024. Earnings per share for the first quarter of fiscal year 2026 was $0.84, compared with $0.73 for the quarter ended June 30, 2025, and $0.72 for the quarter ended September 30, 2024.

“The strong first quarter of fiscal year 2026 results reported here reflect deposit balance and organic loan growth. While total new loan commitments booked in the first quarter of fiscal year 2026 were slightly below the previous quarter, they were $44.5 million, or 102.3%, higher than the first quarter of fiscal 2025. Comparing the first quarter of fiscal year 2026 to the same prior year period, commercial loan production increased 141.9%, mortgage production increased 82.3%, installment lending increased 49.4%, and equity line commitments increased 178.6%. Combined with higher average credit line balances, these increases resulted in a 10.5% annualized growth rate of loan balances in the first quarter of fiscal year 2026. Based on the current pipelines, we expect consistent loan growth through the remainder of the 2026 fiscal year. The loan growth experienced during the first quarter of fiscal year 2025 was supported by a $32.8 million increase in deposit balances obtained through the branch network. Net charge-offs of 0.04% and total delinquency of 0.22% reflect strong loan quality, our borrowers’ ability to navigate inflationary pressures, and a history of prudent underwriting practices. The September 2025 cut to the federal funds target rate allowed for a reduction in prime-based loan rates and in variable rate deposit products. Given a constant balance sheet, we expect the net effect of declining rates to have a positive impact on the bank’s net interest margin through the end of the 2026 fiscal year. I am also pleased to report that the previously announced downtown Canton branch opened in September 2025. We expect this location in Canton Millenium Centre to further enhance the bank’s visibility within the business community and to increase the bank’s Stark County market share. Further, we continue to work towards the previously announced first full-service location in Mahoning County. The Boardman office is expected to open in the summer of 2026. We expect these growth opportunities, along with our continued investment in business development and operations staff, to support future asset growth,” said Ralph J. Lober II, President and Chief Executive Officer.

Quarterly Operating Results Overview

Net income was $2.6 million, or $0.84 per share, for the three months ended September 30, 2025, $2.3 million, or $0.73 per share, for the three months ended June 30, 2025, and $2.2 million, or $0.72 per share, for the same prior year period.

Net interest income was $9.5 million for the three-month period ended September 30, 2025, $9.2 million for the three-month period ended June 30, 2025, and $8.0 million for the three-month period ended September 30, 2024. The net interest margin was 3.37% for the quarter ended September 30, 2025, 3.39% for the quarter ended June 30, 2025, and 2.92% for the quarter ended September 30, 2024. The yield on average interest-earning assets was 5.06% for the quarter ended September 30, 2025, compared with 5.03% for the quarter ended June 30, 2025, and 4.81% for the quarter ended September 30, 2024. The cost of funds was 2.29% for the quarter ended September 30, 2025, compared with 2.23% for the quarter ended June 30, 2025, and 2.56% for the quarter ended September 30, 2024. The reduction in the cost of funds from the prior year period was primarily the result of lower time deposit costs because of recent declines in shorter-term market interest rates.

The provision for credit losses was $285 thousand for the three-month period ended September 30, 2025, and included a $320 thousand provision for credit losses on loans and a reduction of $35 thousand to the reserve for unfunded commitments. This compares with a $32 thousand provision for credit losses for the three-month period ended September 30, 2024, which included a $77 thousand provision for credit losses on loans and a reduction of $45 thousand to the reserve for unfunded commitments. Net charge-offs of $81 thousand were recorded for the three-month period ended September 30, 2025, compared with $59 thousand that were recorded for the three-month period ended September 30, 2024.

Other income increased by $76 thousand, or 5.5%, for the three-month period ended September 30, 2025, compared to the same prior year period primarily due to an increase of $53 thousand, or 8.6%, in debit card interchange income and an increase of $16 thousand, or 17.4%, in bank owned life insurance earnings because of the purchase of new life insurance policies during the 2026 fiscal year.

Other expenses increased by $930 thousand, or 13.9%, for the three-month period ended September 30, 2025, compared to the same prior year period. The increases were primarily in salaries and benefits, occupancy and software expenses, and marketing expenses for the three-month period ended September 30, 2025, compared with the same prior year period, as the Company continues to grow its branch network.

Balance Sheet and Asset Quality Overview

Total assets were $1.19 billion as of September 30, 2025 and $1.17 billion as of June 30, 2025. From June 30, 2025 to September 30, 2025, total loans increased by $21.4 million, or an annualized 10.5%, and total deposits increased by $32.8 million, or an annualized 12.7%.

Non-performing loans were $964 thousand as of September 30, 2025, of which $332 thousand is guaranteed by the Small Business Administration. Excluding the guaranteed portion, non-performing loans were $632 thousand, or 0.08% of total loans, as of September 30, 2025, and $699 thousand, or 0.09% of total loans as of June 30, 2025. The allowance for credit losses (ACL) as a percentage of total loans was 1.04% as of September 30, 2025 and June 30, 2025.

Consumers provides a complete range of banking and other investment services to businesses and clients through its twenty-two full-service locations and one loan production office in Carroll, Columbiana, Jefferson, Mahoning, Stark, and Summit counties in Ohio. Its market includes these counties as well as the sixteen contiguous counties in northeast Ohio, western Pennsylvania, and northern West Virginia. Information about Consumers National Bank can be accessed on the internet at https://www.consumers.bank.

Forward-Looking Information

This press release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 (“PSLRA”). The words “may,” “continue,” “estimate,” “intend,” “plan,” “seek,” “will,” “believe,” “project,” “expect,” “anticipate” and similar expressions are intended to identify forward-looking statements. These forward-looking statements cover, among other things, anticipated future revenue and expenses and future plans, objectives and strategies of Consumers. These statements are subject to inherent risks and uncertainties that could cause actual results to differ materially from those anticipated at the date of this press release. Risks and uncertainties that could adversely affect Consumers include, but are not limited to, the following: regional and national economic conditions becoming less favorable than expected, resulting in, among other things, high unemployment rates; rapid fluctuations in market interest rates could result in changes in fair market valuations and net interest income, pricing and liquidity pressures may result; a deterioration in credit quality of assets and the underlying value of collateral could prove to be less valuable than otherwise assumed or debtors being unable to meet their obligations; material unforeseen changes in the financial condition or results of Consumers National Bank’s (Consumers’ wholly-owned bank subsidiary) customers; legal proceedings, including those that may be instituted against Consumers, its board of directors, its executive officers and others; competitive pressures on product pricing and services; the economic impact from the oil and gas activity in the region could be less than expected or the timeline for development could be longer than anticipated; and the nature, extent, and timing of government and regulatory actions. While the list of factors presented here are considered representative, no such list should be considered to be a complete statement of all potential risks and uncertainties. Unlisted factors may present significant additional obstacles to the realization of forward-looking statements. The forward-looking statements included in this press release speak only as of the date made and Consumers does not undertake a duty to update or revise any forward-looking statement, whether as a result of new information, future events or otherwise, except as required by law.