CONSUMERS BANCORP, INC. ANNOUNCES FOURTH QUARTER FY 2025 EARNINGS

Consumers Bancorp, Inc. Reports:

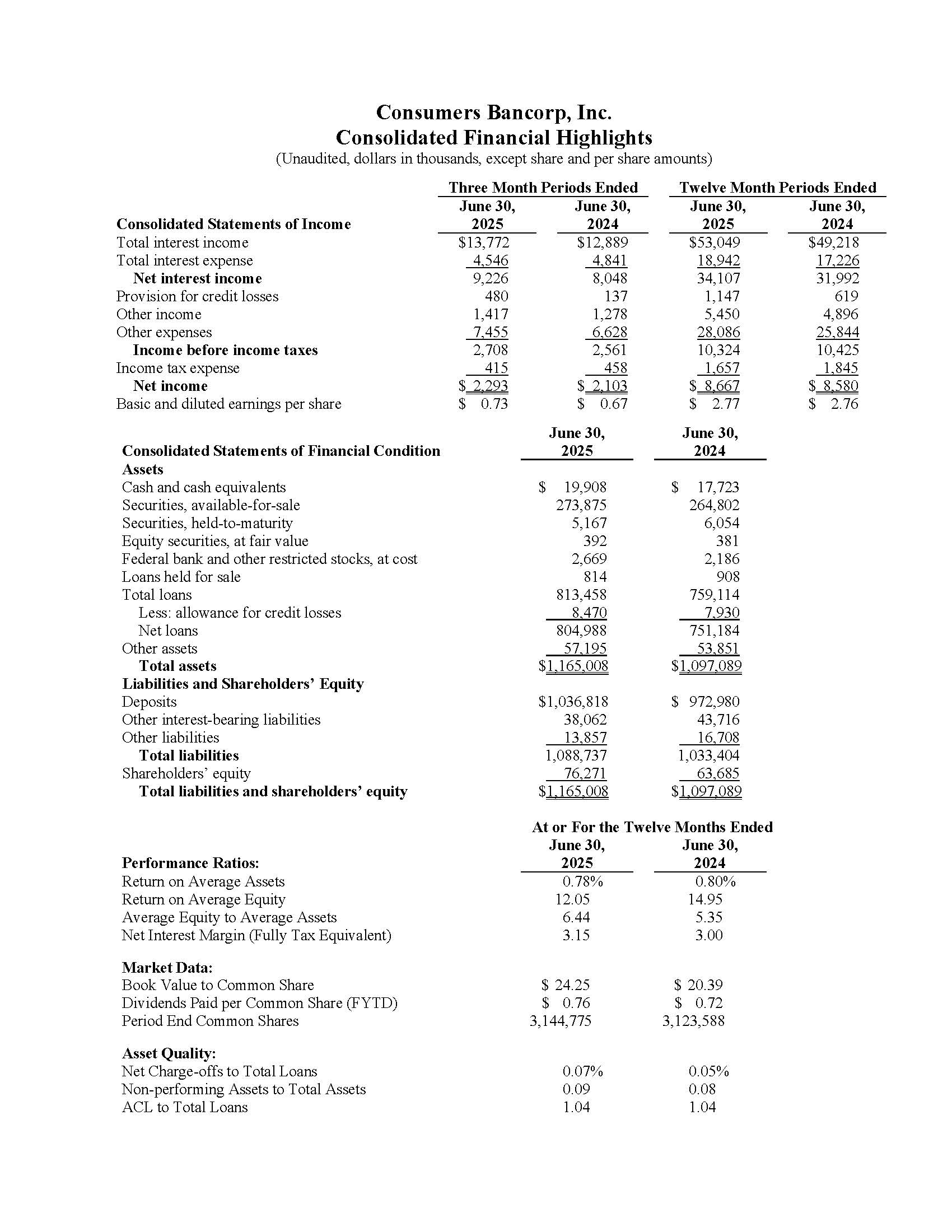

- Net income increased to $2.3 million, or by 9.0%, for the three-month period and to $8.7 million, or by 1.0%, for the twelve-month period ended June 30, 2025 compared with the same prior year periods.

- Total loans increased by $54.3 million, or 7.2%, for the twelve-month period ended June 30, 2025.

- Non-performing loans to total loans were 0.13%, of which 0.04% represents the government guaranteed portion as of June 30, 2025.

- Net charge-offs to total loans for the fiscal year ended June 30, 2025 was 0.07%.

- Total deposits increased by $63.8 million, or 6.6%, for the twelve-month period ended June 30, 2025.

- Shareholders’ equity increased by $12.6 million, or 19.8%, for the twelve-month period ended June 30, 2025.

- Book value increased to $24.25 per share as of June 30, 2025 from $20.39 per share as of June 30, 2024.

Minerva, Ohio—July 29, 2025 (OTCQX: CBKM) Consumers Bancorp, Inc. (Consumers) today reported net income of $2.3 million for the fourth quarter of fiscal year 2025, an increase of $190 thousand, or 9.0%, from the same period last year. Net income increased by $442 thousand, or 23.9%, for the three-month period ended June 30, 2025 compared with the quarter ended March 31, 2025. Earnings per share for the fourth quarter of fiscal year 2025 were $0.73, $0.59 for the quarter ended March 31, 2025, and $0.67 for the quarter ended June 30, 2024.

Net income was $8.7 million, or $2.77 per share, for the twelve months ended June 30, 2025, compared to $8.6 million, or $2.76 per share, for the twelve months ended June 30, 2024. Net interest income increased by $2.1 million, or 6.6%, for the 2025 fiscal year as loans and securities repriced up to higher current market rates and due to the $40.0 million, or 3.9%, increase in average interest earning assets.

“The bank’s 2025 fiscal year end results reflect the investments we continue to make in our infrastructure, sales teams and critical support staff. Additions to our business banking, mortgage, indirect lending, and treasury management teams have contributed to significant balance sheet growth and very strong loan production results. In the 2025 fiscal year, business banking, installment, and residential mortgage related loan originations totaled $269.9 million, a $79.7 million, or 41.9% increase over the 2024 fiscal year. While the new commitments contributed to a higher provision for credit losses in the 2025 fiscal year, these loan balances contributed to an 11.0% increase in organic loan balances over the 2024 fiscal year, providing additional earning assets for future periods. Further, improved performance in residential mortgage, indirect lending, and branch lending allowed those segments to account for nearly half of all organic loan production in the 2025 fiscal year. Credit quality metrics continue to hold strong as borrowers have absorbed higher market rates and inflationary pressures. The total delinquency and nonaccrual ratio decreased to 0.19%, a nine-basis point improvement over the previous year end and the unguaranteed portion of nonperforming assets is a low 0.09% of total loans. Fiscal year 2025 results also reflect the opening of the Massillon, Ohio office, which has reached $10 million in deposits (approximately 1.0% market share) after five months. The bank continues to seek growth opportunities as evidenced by our previously announced de novo offices in Canton, Ohio (Fall 2025) and Boardman, Ohio (Summer 2026). The Canton office, Consumers’ tenth Stark County branch, will serve the central business district and surrounding neighborhoods; a $1.6 billion deposit market. The future Boardman branch, located in a $1.5 billion deposit market, is the bank’s first full-service branch in Mahoning County. It will replace the current Boardman loan production office. We expect these investments to provide future growth opportunities and shareholder value,” said Ralph J. Lober II, President & Chief Executive Officer.

Quarterly Operating Results Overview

Net income was $2.3 million, or $0.73 per share, for the three months ended June 30, 2025 compared with $2.1 million, or $0.67 per share, for the same prior year period.

Net interest income was $9.2 million for the three-month period ended June 30, 2025 and $8.0 million for the same prior year period. The net interest margin was 3.39% for the quarter ended June 30, 2025, 3.27% for the quarter ended March 31, 2025, and 2.99% for the quarter ended June 30, 2024. The yield on average interest-earning assets was 5.03% for the quarter ended June 30, 2025, compared with 4.81% for the same prior year period. The tax-equivalent yield on average interest-earning assets was positively impacted in the fourth quarter of fiscal year 2025 by the transfer of municipal bonds to an investment subsidiary that was formed for the primary purpose of investing in municipal securities. The cost of funds decreased to 2.23% for the quarter ended June 30, 2025, from 2.48% for the same prior year period. The reduction in the cost of funds is a result of recent declines in short-term market interest rates.

The provision for credit losses was $480 thousand for the three-month period ended June 30, 2025, compared with $137 thousand for the same period last year. Net charge-offs of $57 thousand were recorded for the three-month period ended June 30, 2025, compared with $157 thousand that were recorded for the three-month period ended June 30, 2024. The provision for credit losses increased for the three-month period ended June 30, 2025 primarily due to a $45.6 million increase in total loans from March 31, 2025.

Other income increased by $139 thousand, or 10.9%, for the three-month period ended June 30, 2025, compared to the same prior year period primarily due to an increase of $38 thousand in mortgage banking revenue and an increase of $32 thousand, or 45.7%, on bank owned life insurance earnings because of the purchase of a new life insurance policy during the 2025 fiscal year.

Other expenses increased by $827 thousand, or 12.5%, for the three-month period ended June 30, 2025, compared to the same prior year period. Increases in salaries, software expenses, and legal fees all contributed to the increase in other expenses for the three-month period ended June 30, 2025, compared with the same prior year period.

Year-to-Date Operating Results Overview

Net income was $8.7 million, or $2.77 per share, for the twelve months ended June 30, 2025, compared with $8.6 million, or $2.76 per share, for the same prior year period.

Net interest income was $34.1 million for the twelve-month period ended June 30, 2025, and $32.0 million for the same prior year period. The net interest margin was 3.15% for fiscal year 2025, and 3.00% for fiscal year 2024. The yield on average interest-earning assets was 4.90% for the year-to-date period ended June 30, 2025, compared with 4.64% for the same prior year period. The yield on average interest-earning assets increased as loans and securities repriced up to higher current market rates and due to the $40.0 million, or 3.9%, increase in average interest-earning assets. Also, the tax-equivalent yield on average interest-earning assets was positively impacted in the third and fourth quarters of fiscal year 2025 by the transfer of municipal bonds to an investment subsidiary that was formed for the primary purpose of

investing in municipal securities. The cost of funds increased to 2.37% for the year-to-date period ended June 30, 2025, from 2.25% for the same prior year period.

The provision for credit losses was $1.1 million for the twelve-month period ended June 30, 2025, compared with $619 thousand for the same period last year. Net charge-offs of $597 thousand, or 0.07% of total loans, were recorded for the twelve-month period ended June 30, 2025. Net charge-offs of $402 thousand, or 0.05% of total loans, were recorded for the twelve-month period ended June 30, 2024. The provision for credit losses increased in the 2025 fiscal year primarily due to a $80.5 million increase in organic loan growth during the 2025 fiscal year.

Other income increased by $554 thousand, or 11.3%, for the twelve-month period ended June 30, 2025, compared to the same prior year period primarily due to debit card interchange income increasing by $163 thousand, or 7.1%, earnings on bank owned life insurance increasing by $113 thousand, or 40.6%, because of the purchase of a new life insurance policy during the 2025 fiscal year, service charges on deposit accounts increased by $61 thousand, or 3.6%, and mortgage banking revenue increased by $53 thousand, or 15.3%.

Other expenses increased by $2.2 million, or 8.7%, for the twelve-month period ended June 30, 2025, compared to the same prior year period. Increases in salaries, cost of employee benefits, occupancy costs, and legal fees contributed to the increase in other expenses for the twelve-month period ended June 20, 2025, compared with the same prior year period.

Balance Sheet and Asset Quality Overview

Total assets increased to $1.17 billion as of June 30, 2025 from $1.10 billion as of June 30, 2024. From June 30, 2024, total loans increased by $54.3 million, or 7.2%. Total organic loans increased by $80.5 million, or 11.0%, since total loans were impacted by a third-party residential mortgage warehouse line-of-credit that had an outstanding balance of $26.2 million as of June 30, 2024, that was paid down to zero as of June 30, 2025. The paydown was a result of lower mortgage volume due to higher mortgage rates and the funding needs of the lead bank. The outstanding balance of this line-of-credit is expected to increase in future periods if mortgage volume increases and as the funding needs of the lead bank changes.

Total deposits increased by $63.8 million, or 6.6% to $1.04 billion as of June 30, 2025. Total shareholders’ equity increased to $76.3 million as of June 30, 2025, from $63.7 million as of June 30, 2024, because of a reduction of $5.8 million in the accumulated other comprehensive loss from the mark-to-market of available-for-sale securities and from net income of $8.7 million for the fiscal year ended June 30, 2025, which was partially offset by cash dividends paid of $2.4 million.

Non-performing loans were $1.0 million as of June 30, 2025, of which $332 thousand is guaranteed by the Small Business Administration. Excluding the guaranteed portion, non-performing loans were $699 thousand, or 0.09% of total loans as of June 30, 2025 and $502 thousand, or 0.07% of total loans as of June 30, 2024. The allowance for credit losses (ACL) as a percentage of total loans was 1.04% as of June 30, 2025 and 2024.

Consumers provides a complete range of banking and other investment services to businesses and clients through its twenty-two full-service locations and one loan production office in Carroll, Columbiana, Jefferson, Mahoning, Stark, and Summit counties in Ohio. Its market includes these counties as well as the sixteen contiguous counties in northeast Ohio, western Pennsylvania, and northern West Virginia.

Information about Consumers National Bank can be accessed on the internet at https://www.consumers.bank.

Forward-Looking Information

This press release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 (“PSLRA”). The words “may,” “continue,” “estimate,” “intend,” “plan,” “seek,” “will,” “believe,” “project,” “expect,” “anticipate” and similar expressions are intended to identify forward-looking statements. These forward-looking statements cover, among other things, anticipated future revenue and expenses and future plans, objectives, and strategies of Consumers. These statements are subject to inherent risks and uncertainties that could cause actual results to differ materially from those anticipated at the date of this press release. Risks and uncertainties that could adversely affect Consumers include, but are not limited to, the following: regional and national economic conditions becoming less favorable than expected, resulting in, among other things, high unemployment rates; rapid fluctuations in market interest rates could result in changes in fair market valuations and net interest income, pricing and liquidity pressures may result; a deterioration in credit quality of assets and the underlying value of collateral could prove to be less valuable than otherwise assumed or debtors being unable to meet their obligations; material unforeseen changes in the financial condition or results of Consumers National Bank’s (Consumers’ wholly-owned bank subsidiary) customers; legal proceedings, including those that may be instituted against Consumers, its board of directors, its executive officers and others; competitive pressures on product pricing and services; the economic impact from the oil and gas activity in the region could be less than expected or the timeline for development could be longer than anticipated; and the nature, extent, and timing of government and regulatory actions. While the list of factors presented here is considered representative, no such list should be considered to be a complete statement of all potential risks and uncertainties. Unlisted factors may present significant additional obstacles to the realization of forward-looking statements. The forward-looking statements included in this press release speak only as of the date made and Consumers does not undertake a duty to update or revise any forward-looking statement, whether as a result of new information, future events or otherwise, except as required by law.