Consumers Bancorp, Inc. Reports Earnings Q3 2021

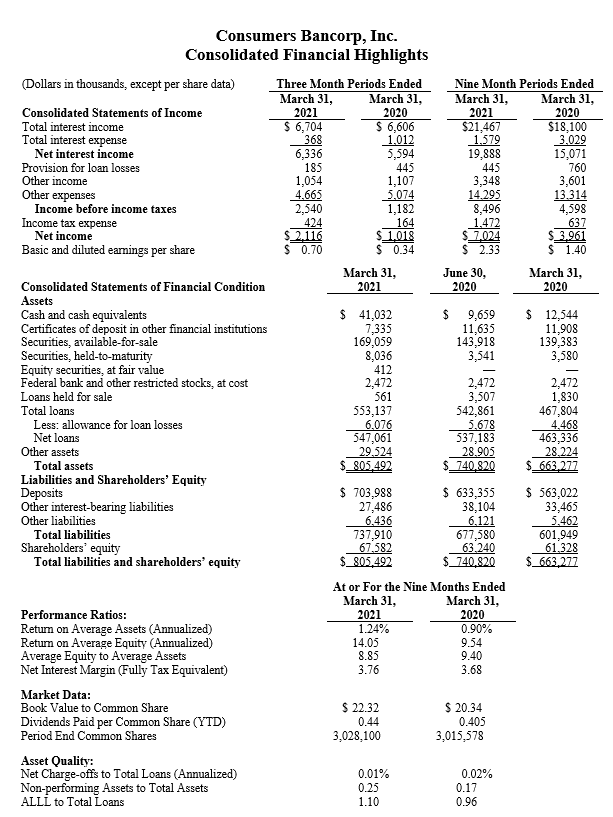

- Net income increased to $2.1 million, or 107.9%, for the three-month period ended March 31, 2021 compared with the same period last year.

- An annualized return on average equity of 12.51% and an annualized return on average assets of 1.11% for the third quarter of fiscal year 2021.

- Total loans increased by $10.3 million, or an annualized 2.5%, for the nine-month period ended March 31, 2021.

- Total deposits increased by $70.6 million, or an annualized 14.8%, for the nine-month period ended March 31, 2021.

- Non-performing loans to total loans of 0.37% at March 31, 2021.

- An increase in the dividend paid per share in March 2021 to $0.15 per quarter which is equivalent to a dividend yield of 3.04% based on the April 15, 2021 market close of $19.74.

Minerva, Ohio— April 19, 2021 (OTCQX: CBKM) Consumers Bancorp, Inc. (Consumers) today reported net income of $2.1 million for the third quarter of fiscal year 2021, an increase of $1.1 million, or 107.9%, from the same period last year. Earnings per share for the third quarter of fiscal year 2021 were $0.70 compared to $0.34 for the same period last year. Net income for the three months ended March 31, 2021 was positively impacted by a $742 thousand, or 13.3%, increase in net interest income, which was primarily the result of a reduction in the cost of funds from the same prior year period. In addition, other expenses for the three-month period ended March 31, 2020 included merger expenses of $433 thousand pre-tax, or $352 thousand after-tax, from the merger with Peoples Bancorp of Mt. Pleasant, Inc. (Peoples), which closed on January 1, 2020.

“Quarterly earnings were again positively impacted by organic loan growth, residential mortgage income, and the bank’s participation in the Small Business Administration’s (SBA) Paycheck Protection Program (PPP). The low interest rate environment continues to drive high residential refinance activity. While the resale market is extremely active, demand for housing far exceeds the current housing supply reducing our opportunity for closed purchase transactions and increasing residential construction and bridge financing,” said Ralph J. Lober II, President and Chief Executive Officer. He continued with, “the PPP lending has been strong since the program restarted in January. As of March 31, 2021, the bank originated $40.8 million in second round PPP loans, bringing its total to $109.5 million through both rounds of the program. While these originations are reflected in our loan balances, we are experiencing growth of our traditional commercial, residential and consumer loan portfolios and total deposits have increased by an annualized 14.8% over the nine months ending March 31, 2021. As of April 15, 2021, approximately 66% of the $68.7 million advanced during the first round of PPP loans has been forgiven by the SBA. We expect our new Green, Ohio office and expansion into southern Columbiana County with the previously announced acquisition of CFBank’s Calcutta and Wellsville branches, which are expected to close in the third calendar quarter of 2021, to provide access to new consumer, commercial, and agricultural customers. We believe there has been positive market reaction to our announcements and we expect to build upon these developments,” he concluded.

Operating Results Overview

Net income increased to $2.1 million, or $0.70 per share, for the three months ended March 31, 2021 compared to $1.0 million, or $0.34 per share, for the same period in 2020.

Net interest income increased by $742 thousand, or 13.3%, for the three months ended March 31, 2021 compared to the same period last year, with interest income increasing by $98 thousand and interest expense decreasing by $644 thousand. The increase in interest income was the result of a $130.0 million increase in average interest-earning assets from the 2020 fiscal year due to organic loan growth and the origination of PPP loans, which had an average balance of $64.4 million in the third quarter of fiscal year 2021. The decline in interest expense was the result of a reduction in deposit and borrowing costs as a result of lower market interest rates. The net interest margin was 3.56% for the quarter ended March 31, 2021, 3.87% for the quarter ended December 31, 2020, and 3.76% for the quarter ended March 31, 2020. The yield on average interest-earning assets was 3.76% for the quarter ended March 31, 2021 compared with 4.43% for the same prior year period. The cost of funds decreased to 0.30% for the quarter ended March 31, 2021 from 0.92% for the same prior year period.

The provision for loan losses was $185 thousand for the three-month period ended March 31, 2021 compared with $445 thousand for the same period last year. Net charge-offs of $21 thousand were recorded for the three-month period ended March 31, 2021.

Other income decreased by $53 thousand for the three-month period ended March 31, 2021 compared to the same prior year period. Other income for the three-month period ended March 31, 2021 includes a $6 thousand gain on sale of securities compared with a $121 thousand gain for the prior year period. For the three-month period ended March 31, 2021, debit card interchange income increased by $100 thousand, or 27.2%, and gains from the sale of mortgage loans increased by $28 thousand, or 23.1%, from the same prior year period. These increases were partially offset by a decline of $65 thousand, or 18.3%, in service charges on deposit accounts primarily due to a decline in overdraft charges as many eligible individuals have received Economic Impact Payments and consumer spending habits have changed during the pandemic, resulting in fewer overdrafts.

Other expenses decreased by $409 thousand, or 8.1%, for the three-month period ended March 31, 2021 compared to the same prior year period. Other expenses for the three-month period ended March 31, 2020 included $433 thousand of merger expenses as a result of the merger with Peoples that closed on January 1, 2020.

Year-to-Date Operating Results Overview

Net income increased to $7.0 million, or $2.33 per share, for the nine months ended March 31, 2021 compared to $4.0 million, or $1.40 per share, for the nine months ended March 31, 2020.

Net interest income for the nine months ended March 31, 2021 increased by $4.8 million compared to the same period last year, with interest income increasing by $3.4 million and interest expense decreasing by $1.4 million. The increase in interest income was primarily the result of a $164.9 million increase in average interest-earning assets from the 2020 fiscal year. The increase in average interest-earning assets was primarily a result of PPP loans and organic loan growth and as a result of the merger with Peoples.

The net interest margin was 3.76% for the 2021 fiscal year and 3.68% for the 2020 fiscal year. Consumers’ yield on average interest-earning assets was 4.05% for the current fiscal year compared with 4.41% for the prior fiscal year. Consumers’ cost of funds decreased to 0.43% for the current fiscal year from 1.00% for the prior fiscal year. PPP loans had an average balance of $64.8 million for the nine-month period ended March 31, 2021 with a total of $2.2 million of interest and fee income recognized during the nine-month period ended March 31, 2021. As of March 31, 2021, there was a total of $2.1 million of unamortized net fees associated with the PPP loans which will be amortized into income over the life of the loans.

The provision for loan losses decreased by $315 thousand to $445 thousand for the nine-month period ended March 31, 2021 compared with $760 thousand for the same prior year period. Net charge-offs of $47 thousand, or 0.01% of total loans, were recorded for the nine-month period ended March 31, 2021.

Other income decreased by $253 thousand, or 7.0%, for the nine-month period ended March 31, 2021 compared to the same prior year period. Other income for the nine-month period ended March 31, 2020 includes $324 thousand of income recognized as a result of proceeds received from a bank owned life insurance policy claim and a $231 thousand gain on sale of securities. For the nine-month period ended March 31, 2021, gains from the sale of mortgage loans increased by $233 thousand, or 58.5%, and debit card interchange income increased by $226 thousand, or 19.8%, from the same prior year period. These increases were partially offset by a decline of $177 thousand, or 16.3%, in service charges on deposit accounts primarily due to a decline in overdraft charges as many eligible individuals have received Economic Impact Payments and consumer spending habits have changed during the pandemic, resulting in fewer overdrafts.

Other expenses increased by $981 thousand, or 7.4%, for the nine-month period ended March 31, 2021 compared to the same prior year period. The 2021 fiscal year includes the full nine months of expenses associated with the three new office locations and additional staff gained as a result of the merger with Peoples compared with only three months of these expense being included in the prior year period. In addition, incentive accruals and mortgage commissions also increased during the 2021 fiscal year.

Balance Sheet and Asset Quality Overview

Assets as of March 31, 2021 totaled $805.5 million, an increase of $64.7 million, or an annualized 11.6%, from June 30, 2020. From June 30, 2020, total loans increased by $10.3 million, or an annualized 2.5%, and total deposits increased by $70.6 million, or an annualized 14.8%.

Non-performing loans were $2.0 million as of March 31, 2021 and $1.2 million as of June 30, 2020. The allowance for loan and lease losses (ALLL) as a percent of total loans at March 31, 2021 was 1.10% and net charge-offs of $47 thousand were recorded for the nine-month period ended March 31, 2021 compared with an ALLL to loans ratio of 1.05% at June 30, 2020 and net charge-offs of $80 thousand for the nine-month period ended March 31, 2020. As of March 31, 2021, 7 borrowers with an outstanding balance of $89 thousand, in the aggregate, continued to receive payment assistance through the loan modification program that offered principal and interest payment deferrals for a maximum period of up to 180 days.

Consumers provides a complete range of banking and other investment services to businesses and clients through its nineteen full-service locations and one loan production office in Carroll, Columbiana, Jefferson, Stark, Summit and Wayne counties in Ohio. Information about Consumers National Bank can be accessed on the internet at http://www.consumers.bank.

Forward-Looking Information

This press release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 (“PSLRA”). The words “may,” “continue,” “estimate,” “intend,” “plan,” “seek,” “will,” “believe,” “project,” “expect,” “anticipate” and similar expressions are intended to identify forward-looking statements. These forward-looking statements cover, among other things, anticipated future revenue and expenses and the future plans, objectives and strategies of Consumers. These statements are subject to inherent risks and uncertainties that could cause actual results to differ materially from those anticipated at the date of this press release. The COVID-19 pandemic is affecting us, our customers, employees, and third-party service providers, and the ultimate extent of the impact on our business, financial position, results of operations, liquidity, and prospects is uncertain. Other risks and uncertainties that could adversely affect Consumers include, but are not limited to, the following: regional and national economic conditions becoming less favorable than expected, resulting in, among other things, high unemployment rates, a deterioration in credit quality of assets and the underlying value of collateral could prove to be less valuable than otherwise assumed or debtors being unable to meet their obligations; rapid fluctuations in market interest rates could result in changes in fair market valuations and net interest income; pricing and liquidity pressures that may result; material unforeseen changes in the financial condition or results of Consumers National Bank’s (Consumers’ wholly-owned bank subsidiary) customers; unanticipated difficulties or expenditures relating to the merger; legal proceedings, including those that may be instituted against Consumers, its board of directors, its executive officers and others; any failure to meet expected cost savings, synergies and other financial and strategic benefits in connection with the merger within anticipated time frames or at all; the response of customers, suppliers and business partners to the merger; competitive pressures on product pricing and services; the economic impact from the oil and gas activity in the region could be less than expected or the timeline for development could be longer than anticipated; and the nature, extent, and timing of government and regulatory actions. While the list of factors presented here is, and the Risk Factors starting on page 16 of the registration statement on Form S-4/A filed with the SEC on September 4, 2019 related to the merger of Consumers/Peoples, are considered representative, no such list should be considered to be a complete statement of all potential risks and uncertainties. Unlisted factors may present significant additional obstacles to the realization of forward-looking statements. The forward-looking statements included in this press release speak only as of the date made and Consumers does not undertake a duty to update or revise any forward-looking statement, whether as a result of new information, future events or otherwise, except as required by law.